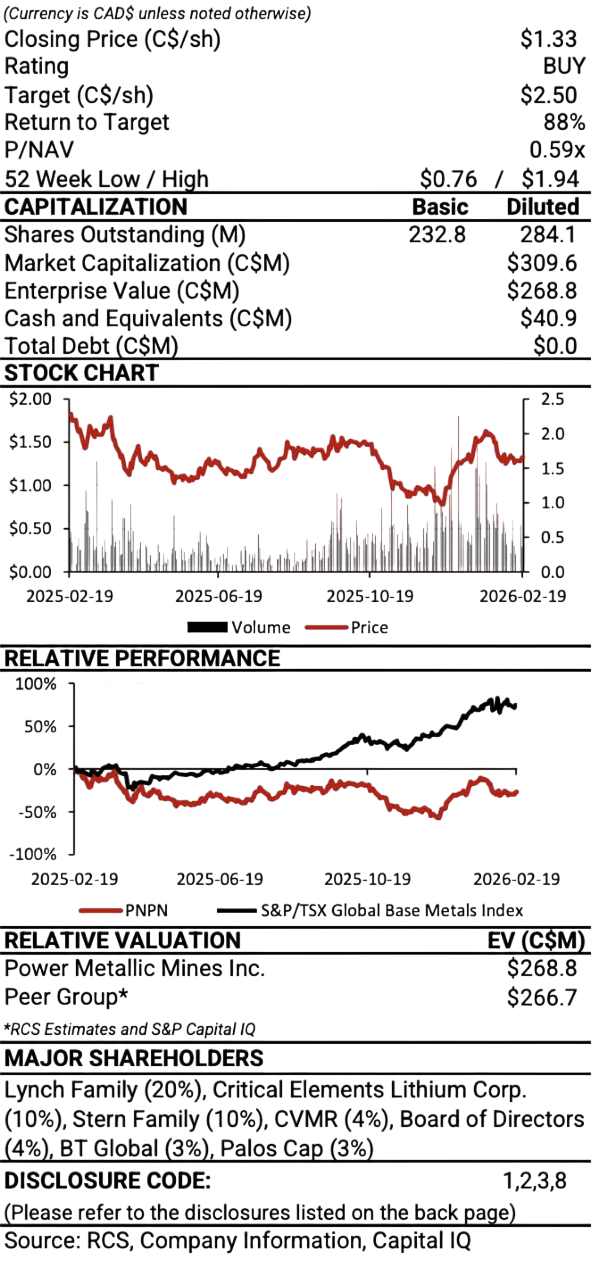

Insights & Resources

Company Description

Power Metallic Mines Inc. is a Canadian exploration company prospecting for nickel, copper and other battery metals in Canada and Chile. It is actively advancing its Nisk property in Quebec, which is host to a high-grade Ni-Cu-Co-PGM sulphide deposit. Beyond Nisk, Power Metallic indirectly has an interest in significant land packages in British Columbia and Chile, by its 50% share ownership position in Chilean Metals Inc. It also owns 100% of Power Metallic Arabia which owns 100% interest in the Jabul Baudan exploration license in Saudi Arabia’s Jabal Sayid Belt.

Power Metallic (PNPN) reported additional assays for five in-fill holes at the Lion Zone at its 80%-owned Nisk polymetallic project in Quebec. The drilling was designed to test plunge extensions of known high-grades and to expand the deposit footprint. The success of this campaign together with the recent excellent metallurgical test results bode well for a maiden mineral resource estimate at Lion. The geologic lines of evidence continue to suggest opportunity for a world-class Ni-Cu-PGE deposit on the property. Multiple new geophysical targets have been identified south of Lion on the recently acquired Quebec Hydro claims. PNPN continues to advance their exploration effort with six drill rigs.

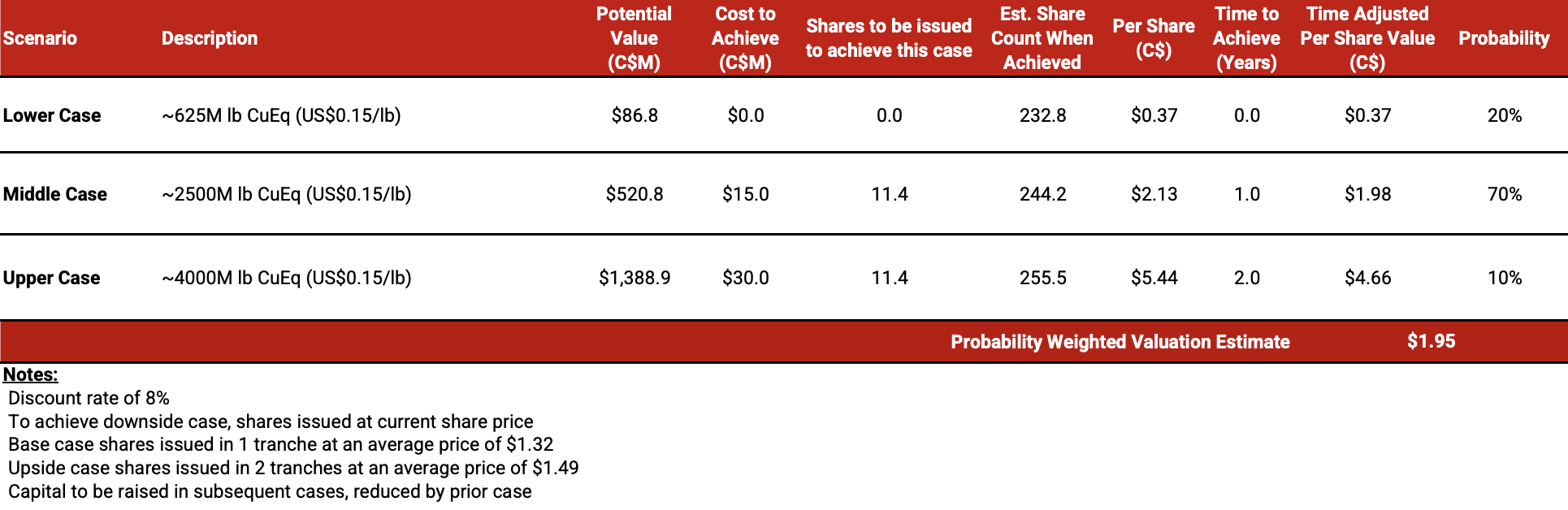

We maintain our BUY rating and target price of C$2.50/sh. Our valuation is based on a probability-weighted assessment of the in-situ resource potential on the Nisk property ranging from a low end of 1.0B lbs CuEq to a maximum of 6.7B lbs CuEq together with the current cash and other project interests. Upcoming catalysts: 1) Updates from the current 100,000m drill program, 2) Mineralogical and preliminary metallurgical testing of the Lion Zone, and 3) Updates from other PNPN projects.

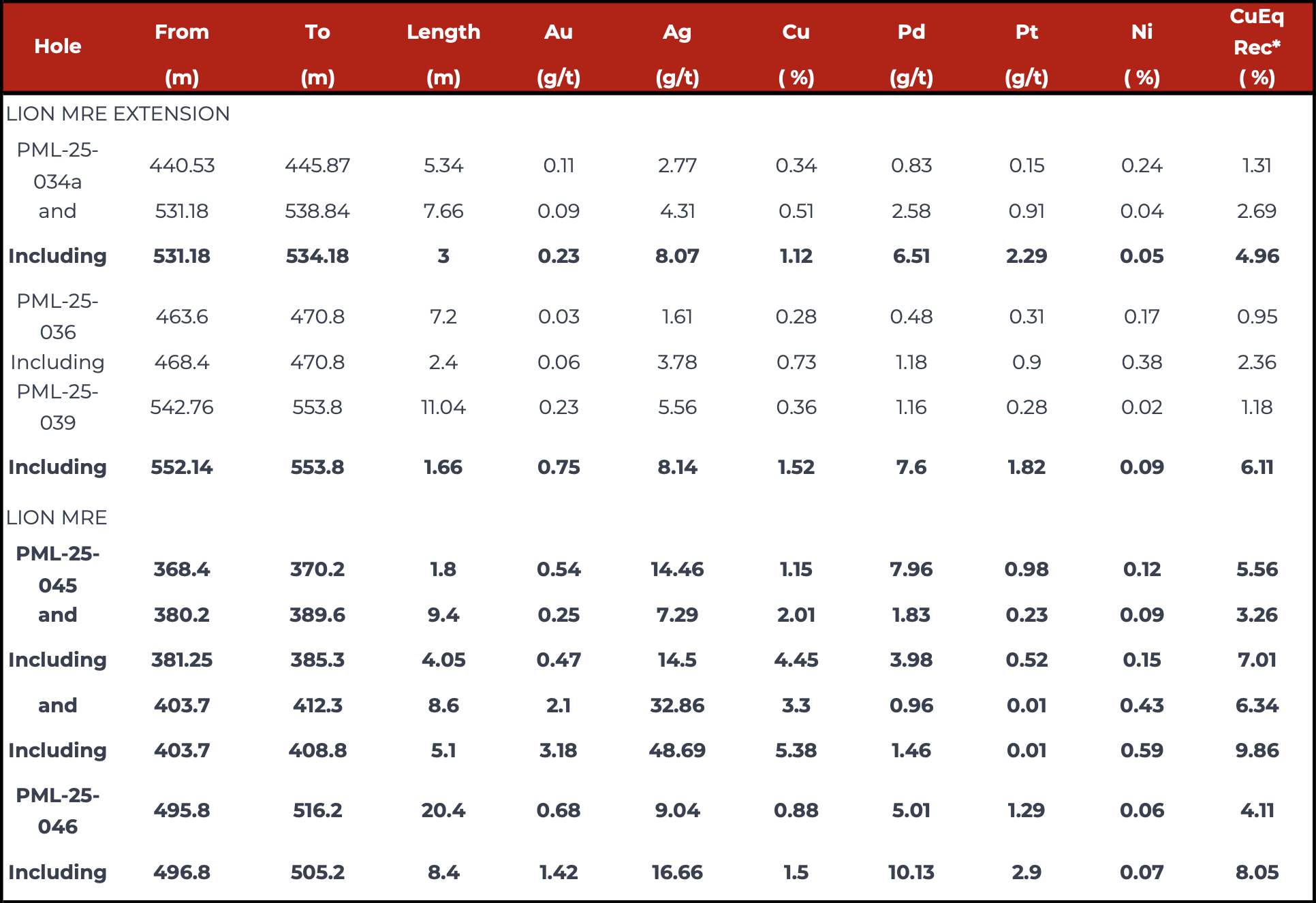

Figure 1:

Lion zone intersections reported in this news release

Source: Company Reports

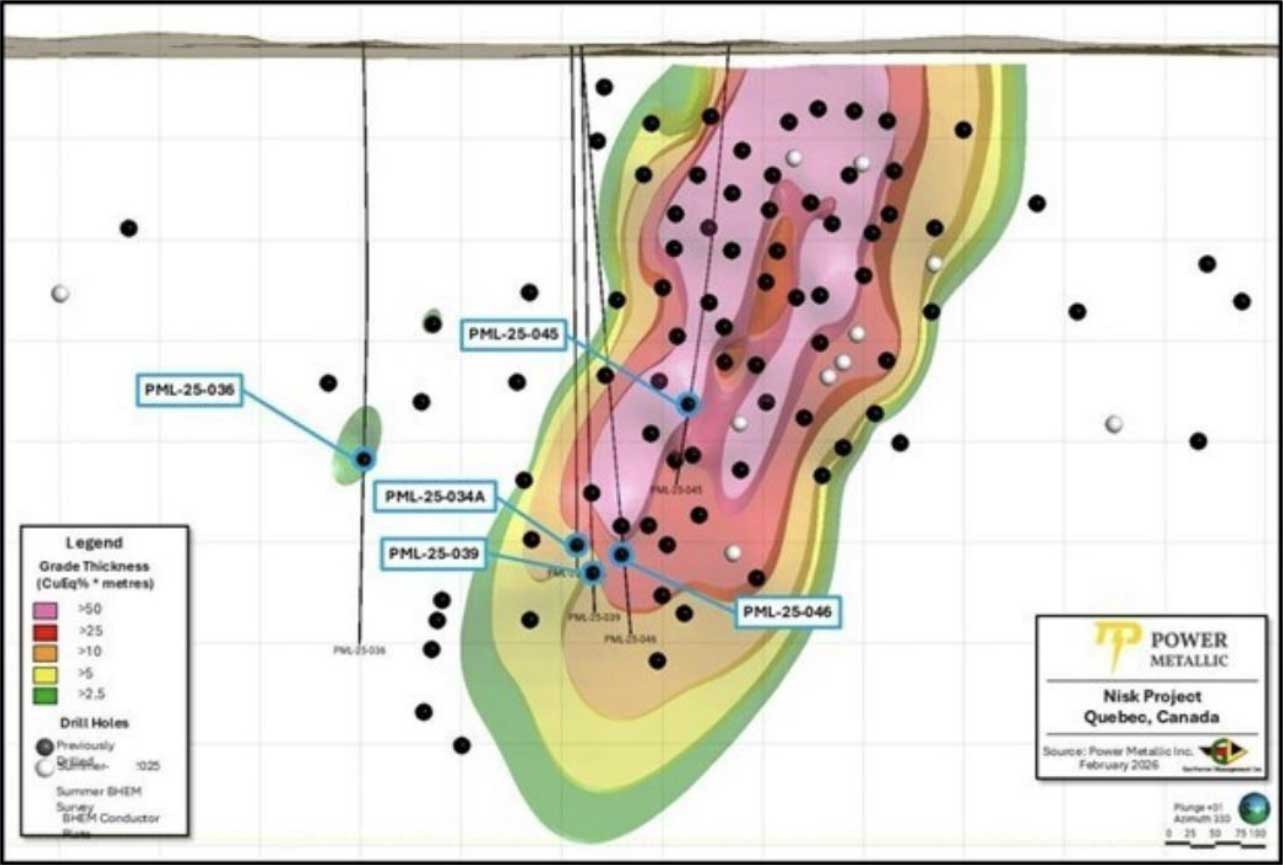

Figure 2: Lion Drill holes reported in this news release, with off-hole BHEM anomalies from recent drilling

Source: Company Reports

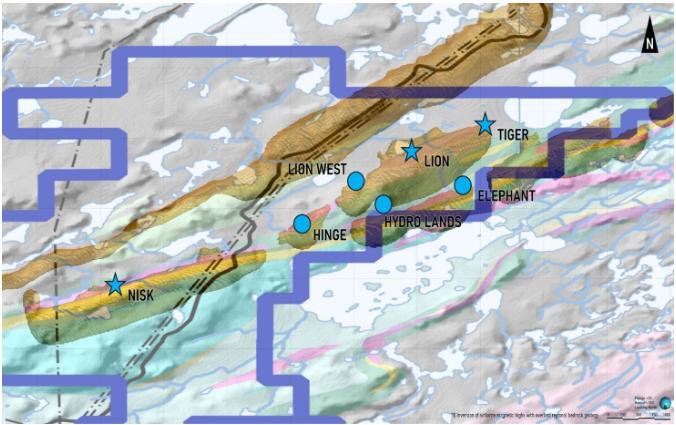

Figure 3: Exploration targets being explored on the Nisk project

Source: Company Reports

Figure 4: A brief overview of historical drilling stats at the Lion zone

Source: RCS Estimates

Figure 5: Probability weighted valuation estimate for Nisk

Source: RCS Estimates

Ron Stewart | MD, Mining Analyst

Daniel Kozielewicz | Research Associate

Shikhar Sarpal | Research Associate

Alex Riazanov, CFA | Research Associate

Red Cloud Securities Inc.

120 Adelaide Street West, Suite 1400

Toronto ON, M5H 1T1

research@redcloudsecurities.com

www.redcloudresearch.com

Disclosure Statement

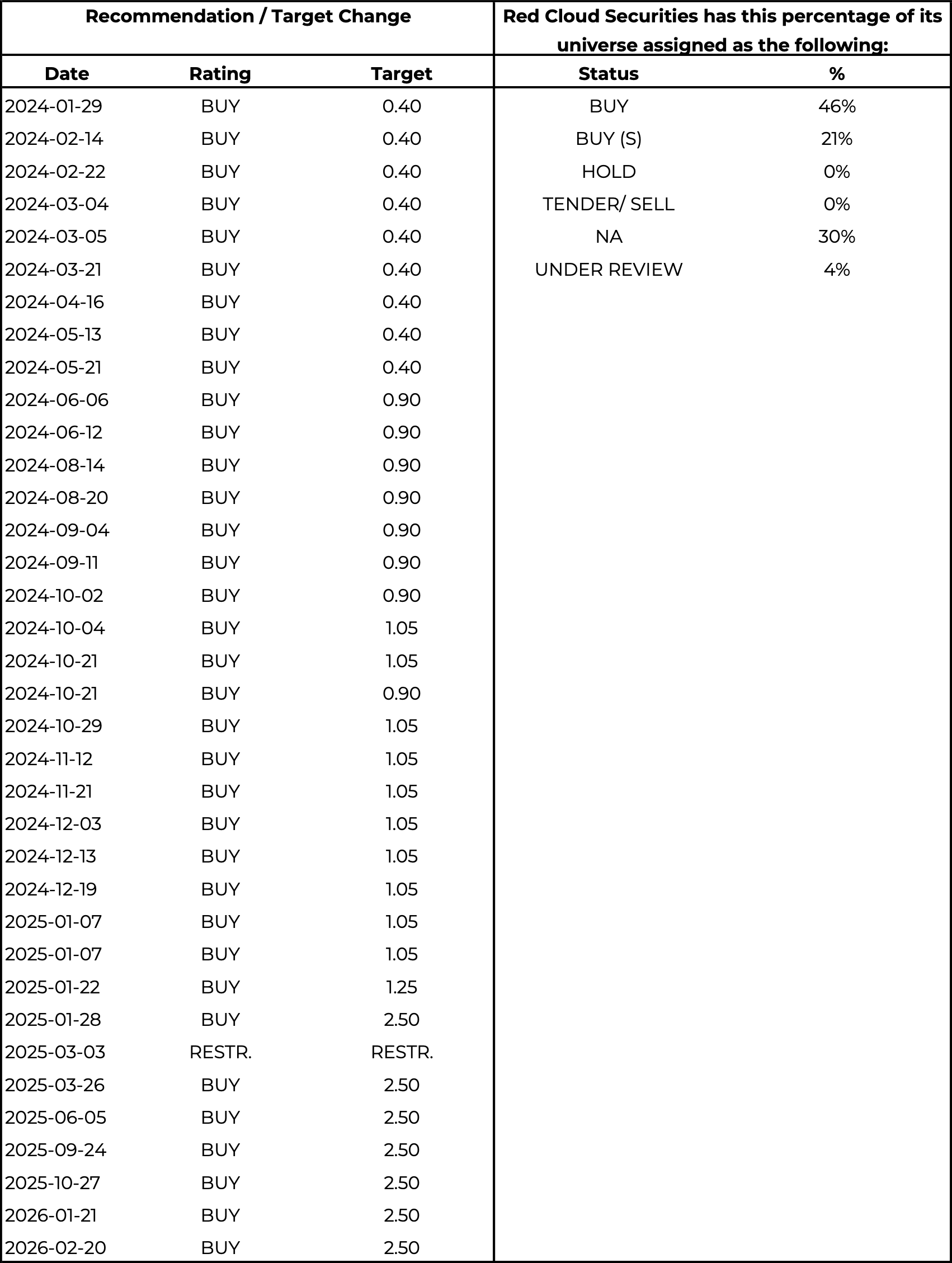

Updated February 20, 2026

Disclosure Requirement

Red Cloud Securities Inc. is registered as an Investment Dealer and is a member of the Canadian Investment Regulatory Organization (CIRO). Red Cloud Securities registration as an Investment Dealer is specific to the provinces of Alberta, British Columbia, Manitoba, Ontario, Quebec, and Saskatchewan. We are registered and authorized to conduct business solely within these jurisdictions. We do not operate in or hold registration in any other regions, territories, or countries outside of these provinces. Red Cloud Securities bears no liability for any consequences arising from the use or misuse of our services, products, or information outside the registered jurisdictions.

Part of Red Cloud Securities Inc.’s business is to connect mining companies with suitable investors. Red Cloud Securities Inc., its affiliates and their respective officers, directors, representatives, researchers and members of their families may hold positions in the companies mentioned in this document and may buy and/or sell their securities. Additionally, Red Cloud Securities Inc. may have provided in the past, and may provide in the future, certain advisory or corporate finance services and receive financial and other incentives from issuers as consideration for the provision of such services.

Red Cloud Securities Inc. has prepared this document for general information purposes only. This document should not be considered a solicitation to purchase or sell securities or a recommendation to buy or sell securities. The information provided has been derived from sources believed to be accurate but cannot be guaranteed. This document does not take into account the particular investment objectives, financial situations, or needs of individual recipients and other issues (e.g. prohibitions to investments due to law, jurisdiction issues, etc.) which may exist for certain persons. Recipients should rely on their own investigations and take their own professional advice before investment. Red Cloud Securities Inc. will not treat recipients of this document as clients by virtue of having viewed this document.

Red Cloud Securities Inc. takes no responsibility for any errors or omissions contained herein, and accepts no legal responsibility for any errors or omissions contained herein, and accepts no legal responsibility from any losses resulting from investment decisions based on the content of this report.

| Company Name | Ticker Symbol | Disclosures |

|---|---|---|

| Power Metallic Mines Inc. | TSXV:PNPN | 1,2,3,8 |

Analysts are compensated through a combined base salary and bonus payout system. The bonus payout is determined by revenues generated from various departments including Investment Banking, based on a system that includes the following criteria: reports generated, timeliness, performance of recommendations, knowledge of industry, quality of research and client feedback. Analysts are not directly compensated for specific Investment Banking transactions.

Red Cloud Securities Inc. recommendation terminology is as follows:

Companies with BUY, HOLD or SELL recommendations may not have target prices associated with a recommendation. Recommendations without a target price are more speculative in nature and may be followed by “(S)” or “(Speculative)” to reflect the higher degree of risk associated with the company. Additionally, our target prices are set based on a 12-month investment horizon.

Red Cloud Securities Inc. distributes its research products simultaneously, via email, to its authorized client base. All research is then available on www.redcloudsecurities.com via login and password.

Any Red Cloud Securities Inc. research analyst named on this report hereby certifies that the recommendations and/or opinions expressed herein accurately reflect such research analyst’s personal views about the companies and securities that are the subject of this report. In addition, no part of any research analyst’s compensation is, or will be, directly or indirectly, related to the specific recommendations or views expressed by such research analyst in this report.